NYDIG report reveals a massive $1.3B IBIT Bitcoin block trade as institutional whale activity reshapes ETF market sentiment.

NYDIG Analysis: Why the $1.3B IBIT Block Trade Signals a Major Bitcoin Whale Exit

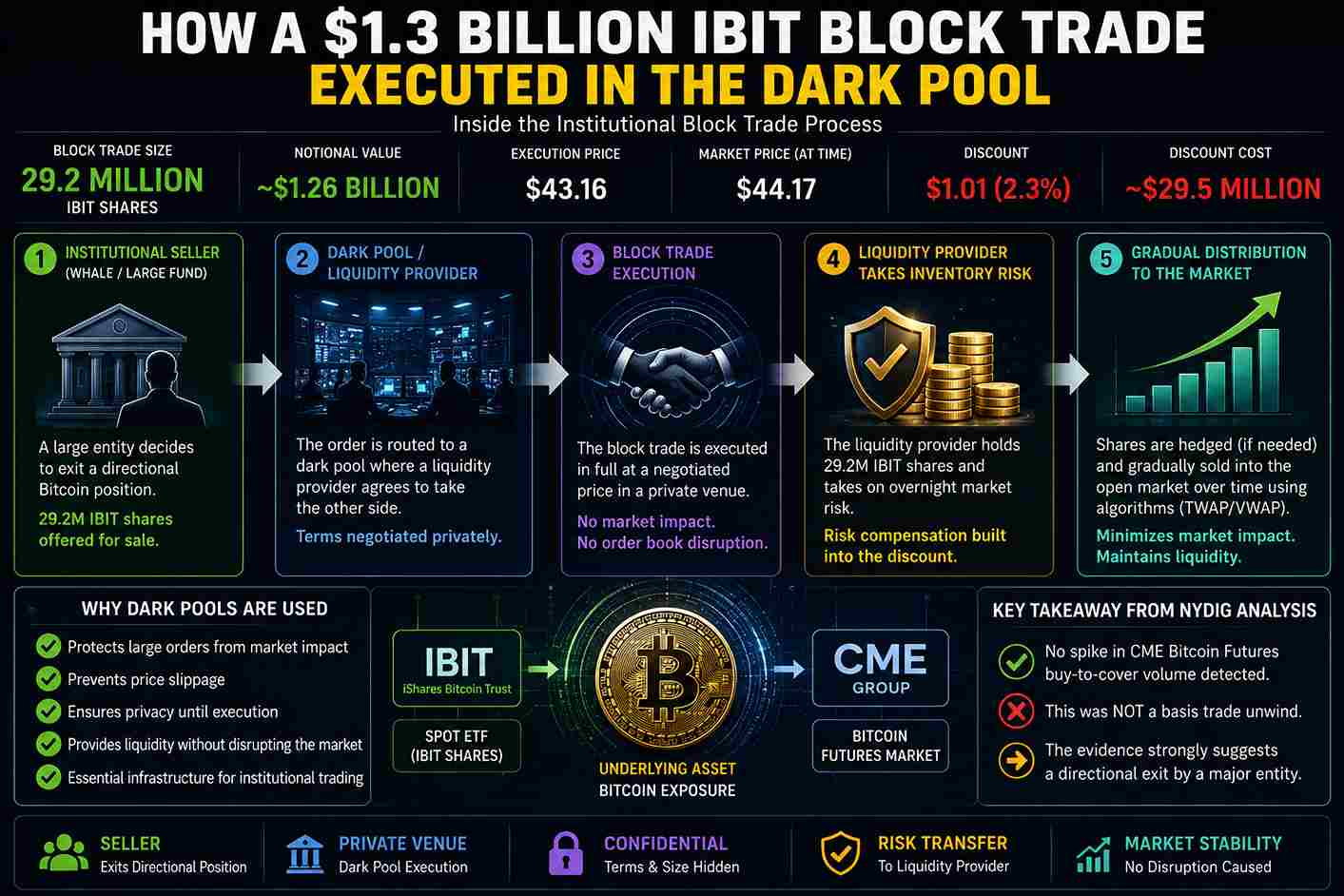

Reading the Institutional Tape: The $1.3 Billion Shockwave

In my analysis of institutional capital flows and ETF market behavior, you quickly learn to follow the money instead of the narrative. Retail traders often obsess over minute-by-minute chart patterns. The real story of the market, however, is consistently written in the block trades. Last week, the cryptocurrency ecosystem experienced a significant liquidity event that demands rigorous analytical scrutiny. A highly concentrated block trade hit BlackRock’s iShares Bitcoin Trust (IBIT). To the untrained eye, this might appear as standard institutional volume in a maturing asset class. The data indicates a far more deliberate reality. According to recent intelligence from NYDIG and its head of research, Greg Cipolaro, this transaction was likely not a routine basis trade unwind. It strongly suggests a prominent entity aggressively unwinding a substantial directional bet on Bitcoin.

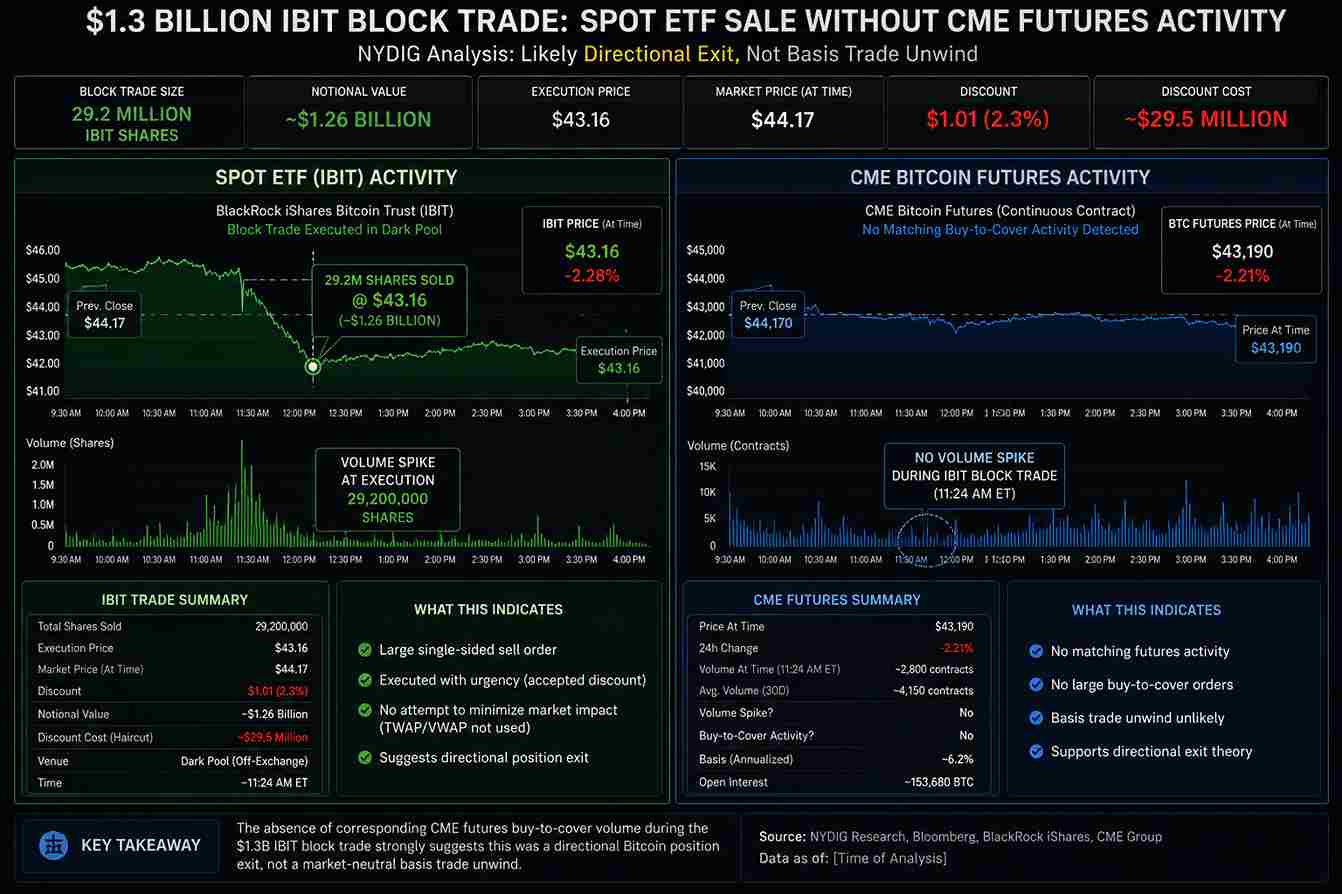

Let us verify the raw numbers, because mathematics remains the only objective truth in capital markets. An unidentified entity sold exactly 29.2 million shares of IBIT in a single transaction. The execution price was roughly $43.16 per share. This brings the total notional value to approximately $1.26 billion, a figure widely reported as $1.3 billion across financial media. This trade was not routed through public exchanges. A market order of that size would have severely disrupted the lit order book and triggered widespread volatility. Instead, it was executed via a dark pool. This private financial forum obscures large-scale transactions from the broader public until the execution is complete.

The execution price represented a $1.01 discount to the prevailing market price of $44.17. When you calculate the impact on 29.2 million shares, that discount translates to a nearly $30 million haircut. The seller willingly abandoned $30 million in capital to secure immediate, guaranteed execution. You do not pay a $30 million urgency premium out of sheer convenience. You pay it because internal metrics dictate an immediate reduction in risk exposure.

Dispelling the Arbitrage Myth: The Missing CME Futures Volume

When a billion-dollar block trade crosses the tape in the Bitcoin ETF sector, mainstream analysts immediately assume it represents the unwinding of a basis trade. The basis trade, or cash-and-carry arbitrage, is a staple strategy among elite hedge funds. It involves buying the spot asset, like IBIT shares, while simultaneously shorting Bitcoin futures on the Chicago Mercantile Exchange (CME). This market-neutral strategy harvests the yield premium between the spot price and the futures price. It completely insulates the fund from the actual price direction of Bitcoin.

If this $1.3 billion sale were simply a hedge fund closing out a basis trade, the mechanical laws of the market dictate a specific footprint. The entity would sell their IBIT shares while simultaneously executing a large buy-to-cover order on their CME short positions. The data indicates a complete absence of this required secondary action. Cipolaro from NYDIG highlighted that there was no corresponding spike in CME Bitcoin futures volume during the time of this block trade.

The absence of this futures volume is a critical indicator. It strongly suggests that the seller was not operating a market-neutral strategy. They were outright long on Bitcoin. They held a directional position, and they opted for a complete exit from that specific allocation. A market-neutral arbitrageur exiting a position is simply moving capital to better yields. A directional whale liquidating a $1.3 billion position is making a high-conviction macroeconomic statement.

Analyzing the Trade Structures: Directional Versus Market-Neutral

To fully grasp the magnitude of NYDIG’s findings, one must understand the distinct operational differences between a directional trade and a market-neutral arbitrage strategy. The core components of each approach illustrate exactly why the data points toward a directional exit.

| Strategy Metric | Directional Trade (The Probable Exit) | Basis Trade (Arbitrage Unwind) |

|---|---|---|

| Primary Objective | Profit directly from the absolute price movement of the underlying asset. | Harvest the yield premium between spot and futures prices. |

| Market Exposure | Fully exposed to the volatility and price direction of Bitcoin. | Market-neutral. Insulated from the price direction of Bitcoin. |

| Execution Footprint | Heavy single-sided volume in the spot or ETF market only. | Simultaneous volume in both the spot ETF and CME futures markets. |

| Urgency Profile | High urgency during risk-off events. Often accepts heavy execution discounts. | Low urgency. Typically unwound smoothly at futures contract expiration. |

| Data Confirmation | Lack of CME futures volume confirms unilateral spot liquidation. | Corresponding CME futures buy-to-cover volume confirms an unwind. |

The Mechanics of the Urgency Premium and Dark Pools

To truly understand the gravity of a $30 million discount, we must examine institutional execution strategies. When a large asset manager or pension fund offloads a billion-dollar position, they rarely execute a single market order. Doing so causes catastrophic slippage. Instead, they utilize algorithmic execution systems like Time-Weighted Average Price (TWAP). These systems break the order into thousands of smaller trades. They trickle them into the market over days to minimize impact and optimize the exit price.

This seller completely bypassed algorithmic execution. They negotiated a block trade with a liquidity provider in a dark pool. The liquidity provider took on the immense overnight risk of holding $1.26 billion in IBIT shares. They demanded compensation for absorbing that inventory. That compensation came in the form of a 2.3% discount.

Executing in a dark pool keeps the terms private until the transaction is finalized. This mechanism is essential for maintaining stability in the broader financial system. It prevents institutional repositioning from causing flash crashes in the lit markets. The fact that the Bitcoin ETF market can support dark pool block trades of this magnitude validates the asset class’s integration into traditional Wall Street infrastructure.

Evaluating Institutional Motivations: Why Exit Now?

While the data strongly points to a directional exit, determining the exact intent behind the trade requires a nuanced view. We cannot state with absolute certainty why the entity chose to liquidate at that exact moment. An action of this size is rarely driven by a sudden fear of short-term price action. Institutions operate on strict mandates and comprehensive risk models.

The decision to accept a $30 million discount points to an internal directive rather than an external market panic. Below is a breakdown of the most probable scenarios that trigger this specific institutional behavior.

| Potential Motivation | Institutional Rationale | Probability Factor |

|---|---|---|

| Portfolio Rebalancing | Bitcoin’s price appreciation caused the asset to exceed the fund’s maximum allowed percentage allocation. A forced liquidation was required to return to target weights. | High. Strict compliance mandates often force managers to trim winning positions regardless of market sentiment. |

| Strategic Risk Reduction | A shift in the macroeconomic outlook or internal risk models prompted an immediate move to cash. The entity prioritized liquidity over maximizing the exit valuation. | High. Macro funds frequently execute aggressive risk-off protocols when key economic indicators flash warning signs. |

| Tax-Loss Harvesting | The entity liquidated the position at a loss to offset significant capital gains in another sector of their global portfolio before the end of a fiscal quarter. | Moderate. The timing and the accepted discount align with urgency often seen in corporate tax maneuvering. |

| Margin Pressure | The fund faced severe liquidity demands or margin calls in an entirely different asset class. They used their liquid Bitcoin ETF holdings as a cash source. | Moderate. Highly leveraged multi-strategy funds occasionally use liquid winners to cover illiquid losers. |

The Resilience of the BlackRock Liquidity Moat

The most compelling takeaway from this liquidity event is the structural resilience of BlackRock’s iShares Bitcoin Trust. Prior to the approval of spot Bitcoin ETFs, a $1.3 billion instantaneous market sell order would have devastated global cryptocurrency markets. It would have triggered cascading liquidations across offshore derivatives platforms.

Instead, the IBIT wrapper successfully absorbed the impact. The underlying price of Bitcoin experienced a cautious retreat following the news, but the market structure did not break. The liquidity provider who bought the block of shares at a discount will likely hedge their exposure. They will slowly distribute those shares back into the lit market over time using standard algorithmic execution. This demonstrates that Wall Street has fundamentally altered the liquidity profile of Bitcoin. BlackRock built a liquidity moat capable of absorbing an institutional anchor. For deep-pocketed investors, this serves as the ultimate proof of concept for the spot ETF structure.

Retail Sentiment Versus Institutional Reality

There is a persistent divergence between retail psychology and institutional mechanics. Following the news of this trade, retail trading forums flooded with speculation. Amateurs debated whether this signaled the end of the bull cycle or if the seller possessed insider regulatory information. This emotional thinking causes retail traders to consistently underperform.

Institutions operate on data, risk metrics, and strict capital allocation frameworks. The executing entity understood the prevailing market sentiment. They knew the order books were thin. They did not hold and hope for a retail recovery bounce. They executed their risk parameters and moved on. Massive capital rotation is a natural component of a functioning, mature market. It is an administrative function, not an emotional reaction.

Forward Guidance: Navigating the Coiled Tape

The critical question for the data-driven investor is how to position capital following this liquidity event. The market is currently in a state of coiled tension. Institutional short positions are applying pressure. Funding rates across offshore derivatives platforms reflect division among professional market makers. When a major player exits a directional long position, it inevitably emboldens the short side of the market. [INSERT_INTERNAL_LINK_HERE]

This event is not a structural failure of the Bitcoin thesis. It is a cleansing of the order book. When large allocations are flushed from the market and absorbed by new buyers, it establishes a healthier foundation for future price discovery. The ETF inflow and outflow data over the coming sessions will act as the ultimate arbiter of market direction.

Key Institutional Metrics to Monitor

To navigate the coming weeks, market participants should rigorously track the following data points to anticipate the next major shift:

- CME Open Interest: Sudden spikes will indicate whether new institutional players are establishing fresh basis trades or taking unhedged short positions to force prices lower.

- Dark Pool Print Volume: Actively scan the consolidated tape for subsequent block trades across other spot ETFs. This helps determine if the IBIT trade was an isolated exit or the start of a coordinated, sector-wide rotation.

- Net ETF Flows: Daily inflow and outflow data will reveal if the broader market is successfully absorbing this new supply.

- Offshore Funding Rates: The spread between major exchanges will highlight whether professional market makers are leaning bullish or bracing for a deeper structural correction.

Final Assessment: Respect the Mechanics

The $1.3 billion IBIT block trade identified by NYDIG offers a masterclass in reading institutional order flow. Greg Cipolaro’s assessment is mathematically sound. The absence of CME futures volume strips away the illusion of a routine arbitrage unwind. We witnessed a Wall Street entity pay a $30 million premium to execute an immediate exit from a directional Bitcoin position. They prioritized liquidity over valuation.

The cryptocurrency market is fully integrated into the deepest liquidity pools on the planet. When whales of this magnitude execute trades, they create structural shifts. The BlackRock IBIT wrapper proved its worth by absorbing the blow. The message to the market is clear. Institutional capital is tactical, calculated, and devoid of sentiment.

As you navigate this environment, base your decisions on hard data, verifiable order flow, and structural market mechanics. Subscribe to our institutional data feed below to improve your understanding of institutional market movements and refine your approach to macroeconomic trends.