Elon Musk's technology empire spans SpaceX, Tesla, xAI, Neuralink and advanced robotics initiatives shaping the future through 2030.

Inside Elon Musk’s $1.25 Trillion Empire: AI, SpaceX, Tesla, Neuralink and the Race to 2030

Inside Elon Musk’s 2026 Empire: SpaceX, xAI, Tesla FSD & Net Worth Data

The global industrial footprint managed by Elon Musk operates on a scale of market capitalization and institutional focus that routinely challenges the trajectory of modern commerce. Today, his corporate portfolio is undergoing its most radical structural transformation. In mid-2026, the global discussion surrounding Musk has shifted entirely away from historical biography narratives or basic net worth tracking. New data from private tender offers, corporate filings, and Wall Street analyses are forcing institutional investors to evaluate a singular, complex reality: the consolidation of his artificial intelligence, aerospace, and robotics holdings into an interconnected ecosystem designed to reshape global infrastructure.

Why is institutional capital analyzing Musk’s corporate empire so closely right now? The current economic cycle has brought his privately held operations and publicly traded vehicles to a massive operational crossroad. In May 2026, market attention is fixated on the recent structural alignment of his frontier artificial intelligence lab, xAI, inside the broader capital matrix, shifting consumer vehicle dynamics at Tesla, and highly anticipated public infrastructure roadmaps. This network blends high-margin satellite internet, heavy aerospace engineering, and cash-intensive frontier artificial intelligence labs. At the same time, Tesla is aggressively pivoting from a pure-play electric vehicle manufacturer into an autonomous robotics operator, testing the limits of public market valuation multiples and attracting fresh institutional attention.

Despite retail fascination with his wealth, market data suggests that the true value of his companies relies on systematic engineering execution rather than speculative hype. This premium business and technology analysis strips away the noise to evaluate the current architecture of the Musk empire using verified financial records, corporate earnings statements, and institutional trackers.

Who is Elon Musk in 2026?

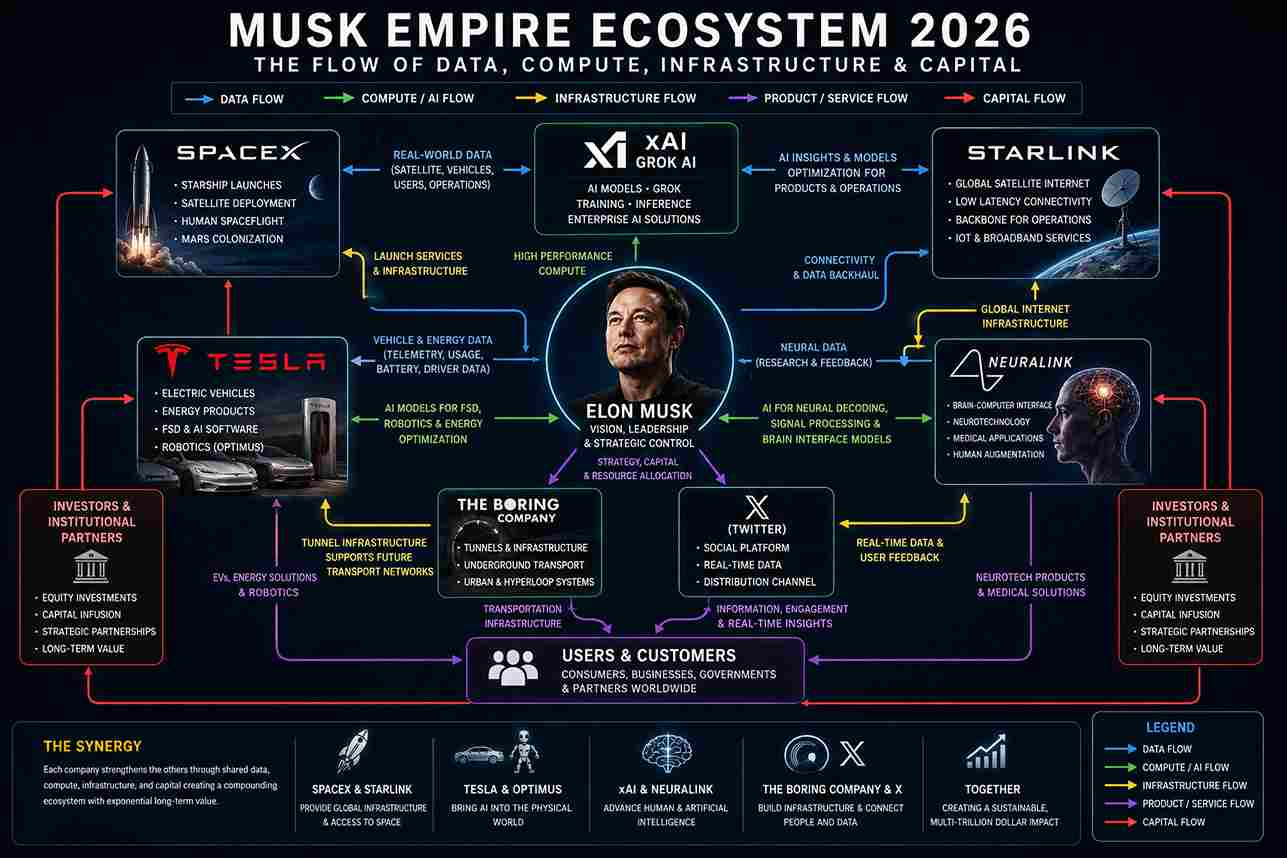

Rather than relying on historical biographies or past personal milestones, evaluating Elon Musk in 2026 requires looking directly at his active operational responsibilities. He sits at the epicenter of five distinct multinational technology and engineering enterprises, managing a corporate network that functions as an interdependent technology stack.

- Tesla Inc. (NASDAQ: TSLA): Musk continues to serve as Chief Executive Officer and Technoking of Tesla. His 2026 focus has shifted significantly from scaling automotive factories to deploying large-scale compute clusters, advancing autonomous driving software, and preparing commercial logistics frameworks for robotic systems.

- SpaceX: As Chief Executive Officer and Chief Designer, Musk directs the technological timeline of the world’s dominant aerospace enterprise. His active operational priorities involve overseeing the rapid orbital launch cadence of the Starship vehicle and expanding the global coverage density of the Starlink satellite constellation.

- xAI: Founded as a direct competitor to established artificial intelligence labs, xAI is led directly by Musk as its Chief Executive Officer. In 2026, he oversees the core optimization of the Grok large language model and coordinates the massive computing infrastructure required to process frontier AI data.

- Neuralink: Operating as the company’s co-founder and primary strategic architect, Musk guides the long-term milestones of this brain-computer interface firm. His active role focuses on navigating regulatory landscapes and defining the technical parameters for the automated surgical systems used to implant medical devices.

- X (formerly Twitter): Following its privatization and subsequent restructuring, Musk functions as the platform’s Executive Chairman and Chief Technology Officer. He dictates the deployment of its backend infrastructure, video streaming protocols, and payment processing features, while positioning X as a vital real-world data training layer for xAI.

According to recent company investor reports and regulatory filings, these roles do not operate in isolation. Musk uses the cash flow, hardware systems, data streams, and engineering talent of each firm to unblock operational bottlenecks across the others, creating a unique corporate structure that presents distinct opportunities and risks for global markets.

Elon Musk Net Worth Breakdown

Evaluating Musk’s net worth requires an analytical approach that looks beyond raw headlines. According to late May 2026 tracking indices, his estimated wealth exhibits a notable variance depending on the valuation methodologies applied to his massive private equity stakes:

Forbes Real-Time Billionaires List: Estimates Musk’s net worth at approximately $828 Billion, driven by real-time modeling of private venture rounds and secondary market tech trends.

Bloomberg Billionaires Index: Positions his net worth at approximately $728 Billion, applying a more conservative discount structure to his tightly held private shares and options packages.

This immense capital base is highly volatile and fluctuates daily based on the public equity market movements of Tesla and the estimated pricing of private secondary market share sales. It is critical to differentiate between paper wealth and true asset liquidity. Musk describes himself as “cash poor” because the vast majority of his wealth is locked up in non-liquid equity inside his companies. To secure operating capital, SEC filings show that Musk has historically pledged a substantial portion of his public Tesla stock as collateral to obtain personal institutional lines of credit.

The composition of his wealth has undergone a massive secular shift over the past two years. While his fortune was previously tied almost entirely to Tesla’s public stock performance, data indicates that more than half of his aggregate wealth is now anchored by his private equity ownership inside SpaceX and the scaling footprint of xAI. The following table breaks down his estimated wealth architecture based on current financial disclosures and cap table tracking.

Elon Musk 2026 Wealth Architecture

| Asset / Equity Holding | Estimated Value Contribution | Ownership Stake Type & Regulatory Source |

|---|---|---|

| Tesla (NASDAQ: TSLA) | ~~$230 Billion to $260 Billion | Common Stock & Restored Compensation Options (SEC Form 4) |

| SpaceX | ~~$310 Billion to $340 Billion | ~~42% Equity / ~~85% Voting Control (Private Tender Offers) |

| xAI / Grok Ecosystem | ~~$45 Billion to $55 Billion | Primary Founder’s Allocation (Venture Capital Filings) |

| X (Formerly Twitter) | ~~$10 Billion to $15 Billion | ~~79% Private Controlling Interest (Schedule 13D Filings) |

| Neuralink & Boring Co. | ~~$5 Billion to $8 Billion | Majority Control / Early-Stage Venture Class (PitchBook Data) |

SpaceX and Starlink

SpaceX has shifted from a disruptive aerospace challenger into the undisputed infrastructure core of global orbital logistics. In 2026, the company’s operational footprint defines both commercial aerospace and sovereign national security infrastructure. This dominance is anchored by three core divisions operating on a unified balance sheet.

Falcon 9 Dominance and Starship Development

The Falcon 9 and Falcon Heavy launch vehicle systems continue to operate as the industry workhorses, commanding over 80% of the world’s commercial launch volume. This baseline cash flow subsidizes the capital-heavy development of the Starship launch platform. Under active Federal Aviation Administration (FAA) oversight and continuous orbital test flights, Starship has transitioned from early low-altitude tests to sustained orbital insertion attempts. Starship’s massive payload capacity is designed to drastically lower the marginal cost per kilogram to orbit, unblocking Musk’s long-term Mars exploration programs and transforming the economics of heavy space logistics.

Starlink Growth and Financial Performance

While rocket manufacturing captures public interest, Starlink functions as the primary financial engine of the entire enterprise. According to private placement offering circulars and institutional financial tracking, Starlink’s revenue reached approximately $11.4 Billion for full-year 2025, accounting for roughly 61% of total SpaceX top-line performance. This recurring subscription engine provides the predictable cash flow necessary to fund deep-space research without relying on public capital markets. Private institutional models estimate that Starlink’s global subscriber base has surpassed 4.5 million active terminals, expanding heavily into maritime, aviation, and enterprise connectivity markets.

Government and Defense Contracts

SpaceX’s infrastructure is tightly integrated with the United States government. The company continues to execute multi-billion-dollar milestones under NASA’s Artemis Human Landing System (HLS) program, positioning Starship as a mandatory vehicle for the return of human crews to the lunar surface. Concurrently, the Department of Defense has expanded its reliance on SpaceX via the Starshield initiative—a specialized satellite array designed for secure government communications and earth observation. This robust contract backlog provides SpaceX with long-term revenue visibility and a structural buffer against broader commercial contractions.

Tesla in 2026

Public equity analysts are locked in a persistent debate regarding the structural valuation of Tesla. Bears argue the asset should be priced in alignment with global automotive legacy manufacturers, which would imply significant downside. Management, however, treats Tesla as a pure-play artificial intelligence and robotics incubator, a thesis that underpins its current forward multiple.

The EV Business and Q1 2026 Performance

Tesla’s core automotive business faces an intensely competitive global environment, particularly from Chinese electric vehicle manufacturers. According to Tesla’s Q1 2026 financial disclosures, the company reported vehicle deliveries of 358,023 units, reflecting an approximate 6% expansion compared to the matching quarter from the prior year. Production across all manufacturing facilities reached 408,386 units during the quarter, creating an inventory roll-over of approximately 50,357 vehicles. Total automotive revenue stood at $16.23 billion, reflecting ongoing global pricing adjustments, while Tesla’s overall adjusted EBITDA stood at $3.66 billion as the company balanced volume growth against per-vehicle profitability.

Full Self-Driving (FSD) and Robotaxi Blueprints

To offset automotive headwinds, Tesla is deploying massive capital into its autonomous driving software ecosystem. The deployment of Full Self-Driving (FSD) version 14 and its associated firmware updates represents a significant technological shift toward end-to-end neural networks, removing legacy human-coded rules in favor of pure video-trained intelligence. Tesla’s capital expenditures have scaled to expand large-scale AI compute clusters, including the deployment of its Cortex supercomputer cluster in Texas. This infrastructure forms the technical foundation for the purpose-built Cybercab vehicle and unsupervised Robotaxi rides, which entered active testing pilots in specific regional markets like Dallas and Houston in early 2026.

The Energy Division: Megapack and Powerwall Status

Tesla’s Energy Storage segment continues to serve as an infrastructure diversification tool. For the first quarter of 2026, Tesla Energy deployed 8.8 GWh of battery energy storage systems (BESS), reflecting a sharp decline from the record 14.2 GWh deployed in Q4 2025 and a 15% dip year-over-year compared to Q1 2025’s 10.4 GWh. Energy generation and storage revenue stood at $2.40 billion for the quarter. Utility-scale Megapack manufacturing continues to ramp up at the Lathrop Megafactory and the expanding Houston facility to serve utility-scale grid stabilization contracts, while Powerwall deployments stabilize within residential markets to protect long-term margins.

xAI and Grok

Elon Musk launched xAI with a specific dual directive: to build a direct technological counterweight to dominant artificial intelligence labs like OpenAI, Google Gemini, Anthropic, and Meta AI, and to establish a dedicated frontier intelligence layer capable of orchestrating the software models running across Tesla and SpaceX.

The Grok Ecosystem and Private Valuation

The primary consumer and enterprise interface of xAI is the Grok large language model. Grok relies on a distinct competitive advantage: direct data access to the global conversational streams running across the X platform, allowing it to ingest and analyze real-world breaking news faster than models reliant on static web crawls. According to venture capital tracking data from sources like Sacra and CNBC, xAI successfully closed a massive $20 billion Series E funding round, elevating its post-money private valuation to approximately $230 Billion. Prominent investors in the round included Nvidia, Cisco, Fidelity, and various global sovereign wealth vehicles.

The Compute Race: The Colossus Supercomputer

To achieve technical parity with older, established artificial intelligence labs, xAI has executed an unprecedented hardware scaling roadmap. At the core of its development strategy is the “Colossus” supercomputer cluster located in Memphis, Tennessee. Operating on a concentrated array of over 100,000 liquid-cooled Nvidia H100 GPUs, the cluster represents one of the densest computational nodes currently active globally. This massive infrastructure footprint allows xAI to shorten model training cycles significantly, scaling Grok’s context windows and reasoning capacities to compete directly in the enterprise API market.

The financial mechanics of xAI reflect the broader “hyper-burn” trend characterizing the frontier AI sector. Venture capital funding disclosures indicate that while xAI has scaled its annualized revenue run rate (ARR) through premium subscriptions and B2B software licenses, its infrastructure maintenance and electricity costs require a substantial capital deployment, making it a high-risk, high-reward bet within the broader empire portfolio.

Neuralink

While Tesla and SpaceX capture macro financial flows, Neuralink represents Musk’s long-term play on high-barrier healthcare and human-machine interface technology. The company has transitioned from theoretical animal models into active human clinical trials under strict FDA investigational device exemptions.

Brain-Computer Interface Technology and Human Trials

Neuralink’s N1 implant utilizes an array of 1,024 electrodes distributed across 64 ultra-thin threads, surgically placed in the motor cortex. In 2026, the company has expanded its human clinical trial cohorts, collecting extensive telemetry data on how paralyzed individuals control external digital interfaces using neural intent. Financial database trackers like PitchBook estimate Neuralink’s private secondary market valuation between $8.0 Billion and $9.5 Billion based on institutional financing rounds.

The Blindsight Project and Commercial Challenges

Beyond motor control restoration, Neuralink’s active development pipeline centers on the “Blindsight” initiative, a device aiming to restore rudimentary visual processing by directly stimulating the visual cortex. While early testing parameters are positive, commercial challenges remain substantial. The regulatory pathway demands multi-year clinical trial sequences and extensive safety tracking before commercial insurance reimbursement structures can be established. This positions Neuralink as a long-horizon venture capital bet within the broader empire portfolio.

Optimus Robot

To understand why Musk has anchored Tesla’s terminal value to robotics, you have to look at the macroeconomic labor constraints facing global manufacturing centers. The development of the Optimus humanoid platform is designed to directly target structural labor shortages in manufacturing, logistics, and heavy industry.

Current Capabilities and Factory Integration

Moving beyond early static prototypes, Tesla is running pilot programs integrating early production models of the Optimus humanoid robot directly into its automotive assembly lines. These units are deployed to automate highly repetitive, dangerous, or anatomically straining tasks. The commercial objective is to validate the unit economics and reliability of autonomous humanoid labor within internal factories before initiating commercial enterprise distribution channels.

The AI Core Advantage

The competitive advantage of the Optimus platform rests in the direct translation of Tesla’s automotive AI stack. Optimus utilizes the identical vision-based neural networks, real-time spatial processing algorithms, and occupancy network architectures deployed inside Tesla vehicles running FSD. By porting this existing software intelligence into a humanoid form factor, Tesla bypasses the need to train a robotics model from scratch, leveraging millions of miles of physical real-world data already collected by its vehicle fleet.

Musk’s Biggest Future Projects

Prudent portfolio managers must focus strictly on the verified, capital-backed projects currently listed in corporate disclosures. Based on official updates from Tesla, SpaceX, and xAI, the multi-year timeline centers on four macro engineering objectives.

- The Starship Mars Program: SpaceX continues to iterate the Starship launch architecture to prepare for the initial unmanned cargo transit windows to Mars. Capital allocation profiles indicate that unblocking this vehicle remains the primary long-term engineering directive of the aerospace firm.

- The Autonomous Robotaxi Network: Tesla is scaling its internal computing clusters to transition FSD from supervised software to an automated, revenue-generating ride-sharing network, aiming to deploy purpose-built vehicles across approved metropolitan zones.

- Commercial Optimus Distribution: Shifting the humanoid robot platform from internal factory testing to a commercially scalable business-to-business (B2B) product tailored for third-party logistics and warehouse automation.

- xAI Infrastructure Expansion: Scaling compute nodes beyond the initial Colossus supercomputer cluster to train next-generation multimodal models capable of orchestrating complex reasoning workflows.

Major Risks

A rigorous, data-driven analysis must balance growth projections against structural headwinds. Musk’s interconnected corporate operational model introduces compounding risks that could alter terminal values if left unchecked.

1. Key-Man Dependency and Capital Leverage

Every organization within this portfolio is structurally dependent on Musk’s active management, strategic direction, and personal capital allocation. Should he face health complications, severe personal liquidity challenges, or legal restrictions, the valuation multiples across all entities would undergo immediate and aggressive compression. Institutional underwriting desks openly note this key-man risk as a primary disclosures variable inside corporate evaluations.

2. Severe Geopolitical and China Supply Chain Exposure

Tesla remains highly exposed to industrial dynamics inside China, relying on Gigafactory Shanghai for a massive portion of its global manufacturing output and supply chain integration. Any escalation in international trade frictions, implementation of technology export bans, or localized regulatory crackdowns would directly impair Tesla’s margin profiles. Similarly, SpaceX relies heavily on specialized chemical components and rare Earth elements that are subject to rigid global supply chain vulnerabilities.

3. Intense Regulatory and Capital Expenditure Pressures

Operating critical satellite communication networks, advanced aerospace platforms, autonomous driving software, and human brain implants places Musk’s companies under continuous regulatory evaluation by bodies like the FAA, NHTSA, and the FDA. Increased regulatory restrictions could delay project timelines and increase compliance costs significantly. Furthermore, the extreme capital expenditure required to fund concurrent frontier AI training and deep-space rocket testing forces a heavy reliance on continuous private placement capital and institutional confidence.

Comprehensive Portfolio Risk Assessment

| Risk Factor Category | Assigned Impact Level | Assigned Probability | Primary Mitigation Variable |

|---|---|---|---|

| Key-Man Disruption | Critical / High Margin Contraction | Low to Moderate | Corporate Governance Restructuring |

| China Supply Chain Blockade | High Automotive Impact | Moderate | Global Manufacturing Diversification |

| Frontier AI Infrastructure Burn | High Capital Attrition | High | B2B Software ARR Scaling |

| Federal Regulatory Delays (FAA/FDA) | Moderate Schedule Slippage | High | Rigorous Compliance Telemetry |

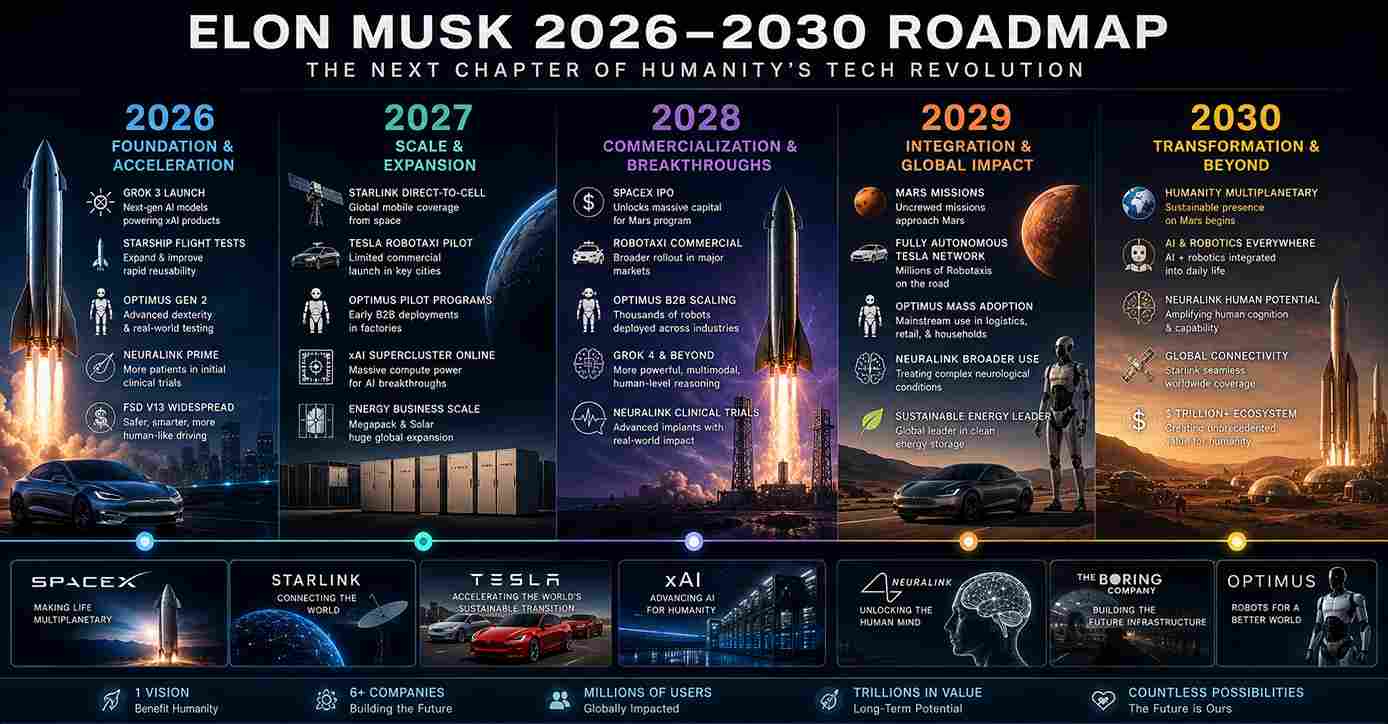

Roadmap to 2030

Looking out toward the end of the decade, the convergence points of the various Musk operations become clearer. The long-term allocation of capital across these entities is designed to form a closed-loop technological ecosystem by 2030. To maintain analytical integrity, it is necessary to separate confirmed company milestones from long-term market speculation.

Verified Corporate Plans

Tesla’s announced manufacturing milestones demand the volume production ramp-up of the Tesla Semi and the Cybercab architecture over the next 24 months. Concurrently, SpaceX is bound by contract to deliver a functional Human Landing System variant of Starship to NASA for the Artemis III and IV lunar missions. In the derivatives and venture capital space, xAI is structurally obligated to achieve clear software licensing scaling targets to justify its recent $20 billion capital injection rounds.

Speculative Possibilities Under Review

In contrast to confirmed contracts, several longer-horizon targets remain subject to immense execution risks. These include the widespread substitution of human warehouse labor with Optimus humanoid units across third-party enterprise supply chains, the establishment of permanent sovereign Martian logistics infrastructure, and the mass consumer commercialization of Neuralink implants for elective neural enhancement. Wall Street models treat these elements as speculative options value rather than core baseline metrics.

Frequently Asked Questions (FAQ)

How much is Elon Musk worth in 2026?

According to tracking data from Forbes, Elon Musk’s net worth is estimated at approximately $828 Billion, while the Bloomberg Billionaires Index positions the figure near $728 Billion. This difference stems from the varying valuation models and discount rates applied to his large, tightly held private equity stakes.

What company contributes most to his wealth?

While his fortune was previously anchored almost exclusively by his public shares in Tesla, the rapid expansion of private markets indicates that his combined holdings in SpaceX and the highly valued xAI venture ecosystem now contribute more than half of his aggregate estimated paper wealth.

Is SpaceX bigger than Tesla?

In terms of public market capitalization, Tesla remains the larger entity, trading on the NASDAQ with a valuation fluctuating around the $740 Billion mark. However, in private equity markets, SpaceX commands a valuation of $200 Billion to $210 Billion based on recent secondary market tender offers, making it the dominant private infrastructure company globally.

What is xAI?

xAI is an artificial intelligence research and development company founded by Elon Musk to build advanced frontier models. Its primary product is the Grok large language model, which features real-time data access to the X platform. xAI recently closed a Series E funding round valuing the private venture at approximately $230 Billion.

What is Optimus?

Optimus is a humanoid robotic platform under development by Tesla. It utilizes the identical computer vision models, spatial processing architectures, and neural network frameworks deployed inside Tesla’s Full Self-Driving vehicle fleet to automate repetitive tasks within manufacturing and logistics environments.

What is Neuralink?

Neuralink is a neurotechnology firm developing implantable brain-computer interfaces (BCIs). The technology utilizes high-density electrode arrays placed in the motor cortex to allow individuals with severe paralysis to operate external computers and digital interfaces directly through neural intent.

What are the biggest risks facing Musk’s empire?

The primary structural risks include concentrated key-man dependency on Musk’s active management, heavy automotive manufacturing supply chain exposure to China, ongoing safety and launch cadence regulatory oversight from agencies like the NHTSA and FAA, and the high capital attrition rate associated with scaling frontier artificial intelligence supercomputers.

Evaluate Portfolio Exposure with Precision

Analyzing modern mega-cap tech ecosystems requires stripping away corporate public relations and relying strictly on verifiable financial metrics, regulatory filings, and market data. Prudent portfolio managers must monitor upcoming private placement cycles, tracking how private markets value frontier technology losses against underlying subscription cash flows. Ensure your investment parameters account for the regulatory, supply chain, and execution dynamics detailed in this structural breakdown before adjusting your technology sector allocations. Stay ahead of institutional capital flows by evaluating verified market metrics and tracking global industry transformations today.

Financial Disclaimer: The business, technology, and financial data detailed in this article are for informational and educational purposes only and do not constitute formal investment, financial, or trading advice. Asset allocations inside volatile technology and frontier engineering markets carry inherent risks of sudden capital loss. Always perform comprehensive independent due diligence or consult with a certified financial advisor before executing portfolio changes.